Facts About Home Renovation Loan Uncovered

Table of ContentsGetting My Home Renovation Loan To WorkA Biased View of Home Renovation LoanAn Unbiased View of Home Renovation LoanSome Known Factual Statements About Home Renovation Loan How Home Renovation Loan can Save You Time, Stress, and Money.

Think about a house improvement loan if you desire to refurbish your house and give it a fresh look. With the assistance of these loans, you may make your home much more aesthetically pleasing and comfy to live in.There are plenty of funding alternatives readily available to aid with your home improvement. The best one for you will depend upon how much you require to borrow and exactly how quickly you intend to pay it off. Brent Differ, Branch Supervisor at Assiniboine Lending institution, supplies some sensible suggestions. "The initial thing you ought to do is obtain quotes from several specialists, so you understand the fair market value of the job you're obtaining done.

The primary benefits of utilizing a HELOC for a home remodelling is the versatility and reduced rates (commonly 1% over the prime rate). Additionally, you will only pay interest on the amount you withdraw, making this a great option if you require to pay for your home restorations in stages.

The major drawback of a HELOC is that there is no set payment schedule. You have to pay a minimum of the passion on a monthly basis and this will certainly raise if prime prices increase." This is a great funding choice for home improvements if you desire to make smaller sized regular monthly payments.

Some Known Incorrect Statements About Home Renovation Loan

Offered the possibly long amortization duration, you can end up paying substantially more rate of interest with a home mortgage refinance compared to other funding options, and the prices connected with a HELOC will certainly likewise use. home renovation loan. A home loan re-finance is properly a new mortgage, and the passion rate could be higher than your existing one

Prices and set-up prices are typically the very same as would certainly pay for a HELOC and you can repay the funding early with no charge. Some of our clients will certainly begin their restorations with a HELOC and after that switch over to a home equity funding once all the prices are validated." This can be a great home renovation financing choice for medium-sized projects.

Personal financing rates are commonly higher than with HELOCs generally, prime plus 3%., the main downside is the passion rate can commonly range between 12% to 20%, so you'll want to pay the equilibrium off rapidly.

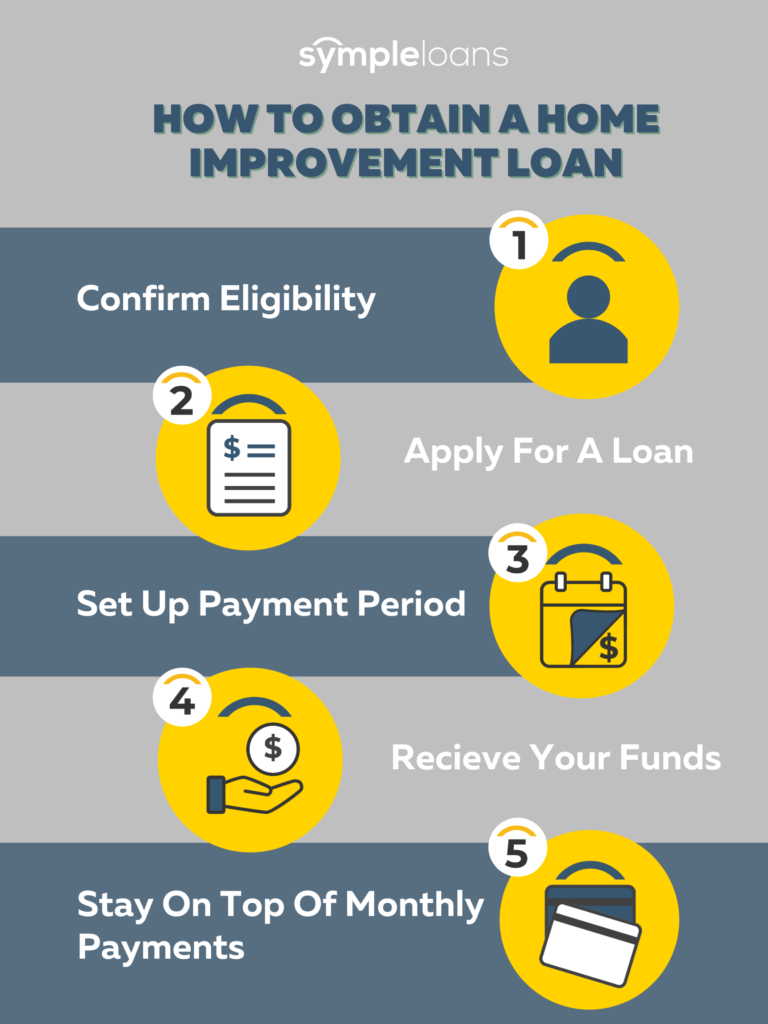

Home restoration car loans are the funding option that enables house owners to refurbish their homes without having to dip right into their savings or spend lavishly on high-interest credit cards. There are check a selection of home remodelling car loan sources readily available to pick from: Home Equity Credit Line (HELOC) Home Equity Financing Mortgage Refinance Personal Lending Bank Card Each of these financing alternatives includes distinct demands, like credit rating, proprietor's revenue, credit line, and interest rates.

Top Guidelines Of Home Renovation Loan

Prior to you start of designing your desire home, you probably want to know the several kinds of home restoration financings available in Canada. Below are several of one of the most usual kinds of home restoration fundings each with its own set of qualities and advantages. It is a kind of home improvement funding that allows home owners to obtain a plentiful sum of money at a low-interest rate.

These are advantageous for massive renovation jobs and have reduced rate of interest than other sorts of personal car loans. A HELOC Home Equity Credit Line resembles a Related Site home equity funding that uses the value of your home as safety and security. It works as a credit rating card, where you can obtain as per your demands to money your home remodelling projects.

To be eligible, you need to possess either a minimum of a minimum of 20% home equity or if you have a home mortgage of 35% home equity for a standalone HELOC. Re-financing your mortgage process entails replacing your existing home mortgage with a new one at a lower rate. It decreases your regular monthly settlements and reduces the quantity of interest you pay over your life time.

Some Ideas on Home Renovation Loan You Need To Know

For this, you may need to provide a clear construction strategy and budget for the remodelling, including determining the cost for all the products needed. Additionally, personal finances can be protected or unsafe with much shorter payback durations (under 60 months) and featured a higher rate of interest rate, depending on your credit report and earnings.

Home Renovation Loan Fundamentals Explained

Shop funding programs, i.e. Shop credit scores cards are supplied by numerous home enhancement shops in Canada, such as Home Depot or Lowe's. If you're preparing for small home enhancement or DIY jobs, such as installing brand-new windows or bathroom improvement, obtaining a shop card with the retailer can be a very easy and quick procedure.